Majors hike Interest Only rates by 30-35 basis points

CBA and NAB have been the most recent of the majors to increase their interest only payment rates.

Since the last decrease of the RBA Cash Rate in August 2016, we have seen tightening qualitative measures from APRA. The banks have indicated they are supportive of the banking regulator’s moves to manage the level of growth and resiliency in the housing market. To meet its regulatory requirements, the banks have announced it will increase variable interest only home loan rates for both owner-occupiers and investors.

Matt Comyn, group executive of retail banking services (CBA), said: “Paying off your home is important for Australians. For owner occupier customers repaying principal and interest, they can take advantage of the interest rate reduction to pay off their home loan faster. These changes also help us keep the right balance in our home loan portfolio, in line with what our regulators require.”

These interest only changes are not in response to the bank levy that was announced as part of the Federal Budget in May, the banks have said but rather tightening qualitative measures from APRA.

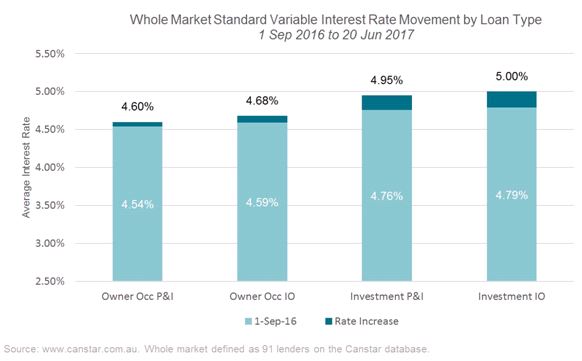

Canstar has interrogated its database to identify the macro-trends in rates since 1st September 2016, a time when the August cash rate cut would have washed through the base data and standard variable rates to better track changes.

Casting our eyes back a little more than 12 months ago, the interest rate regime was pretty straightforward – investment, owner occupied, interest-only and principal and interest were all one rate. Fast forward to today and you will struggle to find this model.

Across the market (the population of 91 Canstar listed lenders) currently the average margin for interest-only investment over principal and interest owner occupied rates is 40 basis points. The trend had started before the 1st September but has since widened from its then 25 basis point.

We would encourage customers who currently make interest only payments to make enquiries into switching to principal and interest repayments if able or viable for their circumstance.

Contact us to see if switching payments and attracting a lower rate is in your best interest.

Donna-Lee Parkes